Advocates outline Social Security expansion act at St. Peter town hall

Brian Rohrenbach discusses provisions of the Social Security Expansion Act, including higher benefits, expanded survivor protections, improved cost-of-living adjustments, and tax changes for high earners designed to strengthen the program’s long-term solvency. (Photo by Amy Zents)

ST. PETER — Supporters of the Social Security Expansion Act met Tuesday at the St. Peter Community Center to outline how the proposed legislation would strengthen the nation’s Social Security system, increase benefits, and ensure long�’term solvency for future generations.

“This is a unifying issue,” Brian Rohrenbach, a longtime Minnesota resident and grassroots advocate, said. “It doesn’t matter what party you belong to. Social Security touches nearly every family in America.”

The forum featured personal stories, economic data, and a detailed explanation of how Social Security functions, countering common misconceptions about the program’s funding and long-term viability.

Rohrenbach emphasized that Social Security is an insurance system — not welfare — designed to protect Americans against loss of income due to retirement, disability, or death.

Rohrenbach shared his own experience receiving survivor benefits after his father died when he was a child. His first monthly Social Security check was $43, an amount that gradually increased over time. His mother saved the benefits, allowing him to have approximately $4,500 when he reached adulthood.

“At that time, Social Security was equated with welfare,” Rohrenbach said. “People didn’t talk about it. Today we understand it as what it really is, an earned entitlement that workers pay into.”

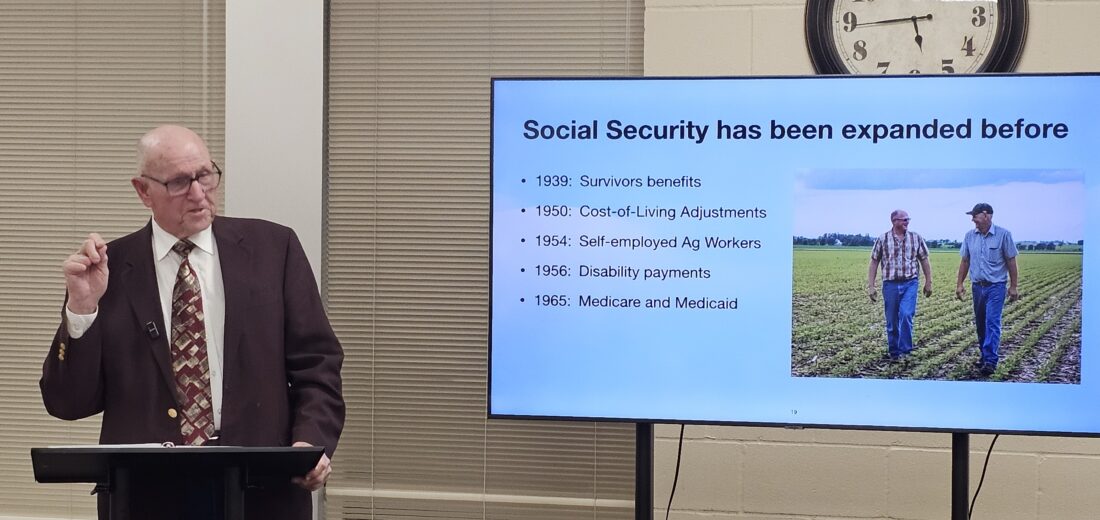

Rohrenbach said Social Security has evolved significantly since its early years, expanding coverage and benefits to more Americans, including agricultural workers and the self-employed.

In the 1950s, farm families became eligible, providing financial security to rural households that often had limited or unstable incomes.

Several personal examples illustrated the program’s role beyond retirement. Rohrenbach described his sister’s husband, who became fully disabled after a severe stroke in his 50s, leaving behind a spouse and three minor children.

“Social Security benefits helped that family survive,” Rohrenbach said. “We didn’t even realize at the time how they were managing until years later.”

According to data shared at the meeting, the average Social Security retirement benefit is nearly $2,000 per month. About 55 million Americans receive retirement benefits, and approximately 40% rely on Social Security as their sole source of income.

“If Social Security didn’t exist, many of these people would have nothing,” Rohrenbach said. “Without it, we’d likely be talking about returning to poor farms.”

The economic impact of Social Security was also highlighted. In Minnesota alone, about $2.2 billion is distributed each month through Social Security benefits, totaling roughly $26 billion annually, an amount comparable to the state’s crop and livestock production value.

“That money isn’t sitting in offshore accounts,” Chuck Smith-Dewey, a supporter of the Social Security Expansion Act, said. “It’s spent at grocery stores, gas stations, pharmacies and cafés on Main Street, not Wall Street.”

Rohrenbach addressed concerns about the Social Security trust fund, explaining that it currently holds a surplus of approximately $2.6 trillion.

He emphasized that Social Security does not contribute to the national debt and has never required a congressional appropriation.

“Funds collected through payroll taxes are dedicated by law to Social Security benefits,” Rohrenbach said. “They can’t be used for anything else.”

The forum addressed projections that the trust fund could be depleted between 2033 and 2035 if no changes are made. Even in that scenario, Rohrenbach said, Social Security would continue paying benefits at about 75% of projected levels as long as workers continue paying payroll taxes.

The Social Security Expansion Act aims to strengthen the system by gradually applying payroll taxes to wages above $250,000, providing beneficiaries with an annual $2,400 increase, and improving cost-of-living adjustments using the Consumer Price Index for the Elderly (CPI-E).

The legislation raises minimum benefits to 125% of the federal poverty line, restores student benefits for children of deceased or disabled workers through age 22, and merges the Disability Insurance and Old Age & Survivors trust funds to ensure long-term financial stability.

Advocates said the legislation would extend Social Security’s solvency for at least 75 years.

“This is not about dismantling the system,” Rohrenbach said. “It’s about strengthening and expanding it.”

Rohrenbach also pushed back against proposals to privatize Social Security, warning that private investment accounts would introduce higher administrative fees and market risks.

“People who want to privatize Social Security want the cash flow, not the responsibility,” Rohrenbach said. “They’re not interested in guaranteeing benefits.”

The forum concluded with a call for civic engagement, urging attendees to contact their congressional representatives and ask whether they support the Social Security Expansion Act.

Rohrenbach said continued public education is critical, particularly among younger generations who often believe Social Security will not be there for them.

“If you’re paying in, you’re insured,” he said. “That protection exists today, not just someday in the future.”

-

- Brian Rohrenbach discusses provisions of the Social Security Expansion Act, including higher benefits, expanded survivor protections, improved cost-of-living adjustments, and tax changes for high earners designed to strengthen the program’s long-term solvency. (Photo by Amy Zents)

Local News

Two ice fishing contests this weekend

Brown Co. Board OKs electronic bidding

NEW ULM — Brown County Commissioners unanimously approved implementing bidVAULT electronic bidding for highway ...

A time for the books

Advocates outline Social Security expansion act at St. Peter town hall

Filzen named Tourism Person of the Year